One thing our clients appreciate about working with us is that we don’t believe in cookie-cutter services or a one-size-fits-all approach. Instead, we follow a meticulous process designed to help get to know each client’s situation, goals, and level of risk tolerance so that we can make appropriate recommendations to meet their needs. Everyone is different and we may amend our approach to suit a specific client, but in general, we utilize the following process to help those we’re privileged to serve.

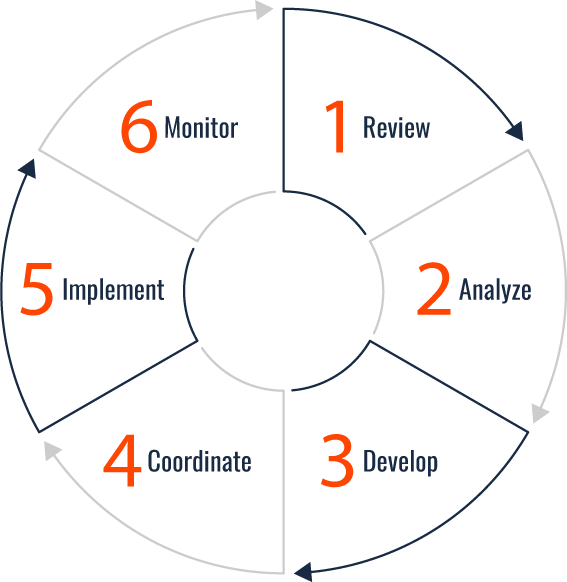

Step 1: Review

Every family's financial situation is unique. That's why it's so important to find out as much as we can about you and your financial goals. The more we know about you, the more precise recommendations we can make and the more we can help you. As a result, we may take some time to discuss your hopes, dreams, and objectives, and the things that really matter to you. This is the basis for the first meeting with anyone we sit down with.

Step 2: Analyze

As needed, we will work with you to identify and prioritize your objectives, and then help establish benchmark goals. This is important because we live in a world of unlimited choices. People often fail to achieve objectives because they try to accomplish too much at once, or they don't attach specific deadlines to their goals. By breaking down your goals to specific objectives, you can look at available resources and decide which goals are realistic, and which should be adjusted and scaled down.

Step 3: Develop

Based on our conversation and analysis, we can recommend the steps that it will take to help you achieve your financial goals.

Step 4: Coordinate

We regularly coordinate insurance and financial activities for clients with the other members of their team of financial, tax, and legal advisors. We can do the same for you.

Step 5: Implement

We'll implement your strategy, and work closely with you and your other third party professionals to ensure its success. We'll monitor progress and provide ongoing service as your needs and situation change over time.

Step 6: Monitor

This is not a one-shot deal. Strategies need to be adjusted periodically as your life and the economy changes. We will work with you over the years to help keep your strategy on track with your changing needs.

Business Solutions

Here at Scheideman Financial Strategies, we offer a wide array of services to help business owners address their financial needs at every stage of the business life cycle. Taking into account their personal values and financial goals, we create and execute customized strategies to help entrepreneurs meet their objectives. Some of our key services are detailed below.

Eagle Strategies LLC, is a Registered Investment Adviser and an indirect, wholly owned subsidiary of New York Life, and is a provider of holistic investment advisory and financial planning services. Our financial advisors leverage Eagle’s sophisticated wealth management platform, comprised of many of today’s leading investment managers, to design customized investment solutions to help address our clients’ unique investment objectives and risk tolerance levels. The breadth and investment knowledge of our Financial Advisors, coupled with Eagle’s diverse team of investment experts, allows them to provide the continuous financial guidance needed to help clients achieve long-term financial success.

All investment advisory services are offered through Eagle Strategies LLC, a registered investment adviser. All investments involve risk, including the potential loss of principal.

Personal Solutions

Scheideman Financial Strategies provides individuals and families with innovative, cutting-edge products and services to help them grow, protect, and conserve their wealth through all stages in life. Taking into account your needs, goals, and tolerance for risk, we will work with you to bring clarity to what you want to achieve and how to get there. Some of our key services are detailed below.

The team members at Scheideman Financial Strategies are trained professionals who can help you identify your financial needs and then determine which financial and insurance products can best help you meet your objectives. Some of the products we often use to serve the needs of our clients include:

Life Insurance

Many people think that life insurance is only for people with families. While it’s true that life insurance can help provide for the needs of dependents, life insurance also can be an important part of a well-thought-out estate, business succession, or charitable giving plan. And permanent life insurance offers many living benefits as well, such as tax-deferred cash value accumulation. For all of these reasons, life insurance can be important for someone starting out—or for someone who's starting over.

An annuity is a unique financial vehicle designed to help you accumulate money for your retirement and/or turn a lump sum into a guaranteed stream of income payments. Deferred annuities offer the advantage of tax deferral and can be used to accumulate money for retirement. Income annuities are used to generate a stream of income payments that are guaranteed to last for as long as you need them to—even for the rest of your life.* Some of the different types of annuities are:

Here at Scheideman Financial Strategies, we are able to help farmers, landowners, and agribusinesses with financial planning and decisions because we understand what it takes to create a successful farming operation, and the challenges in finances that many farmers face. With our assistance and guidance, you can help ensure that your farm and its finances track with your goals going forward.

Landowners, agribusinesses, and farmers need specialized options when it comes to managing their money and protecting their assets. Our goal is to tailor every financial strategy to the needs and goals of the individual in such a way that he or she feels confident with their legacy.

When you leave a job or retire, you have a decision to make regarding your 401(k) money. While leaving those assets in the former employer's plan is an option, a rollover can be a consideration. Working with your tax advisor, we can help you determine the right course of action for you. This may include: leaving the funds in your existing plan, if permitted, or rolling them into your new employer's plan, if one is available and rollovers are permitted. Each choice offers advantages and disadvantages, depending on your specific needs and retirement plan, such as the desired investment options and services, applicable fees, expenses, and withdrawal options, as well as required minimum distributions and tax treatment of applicable options.

Neither New York Life Insurance Company nor its agents offer tax advice.

Asset Protection

There are numerous financial strategies and retirement income strategies that can help you accumulate assets for the future, protect your business and personal assets from liabilities, and safeguard asset transfer to children and grandchildren. We can help you figure out what the right course of action is for your specific situation and objectives.

Charitable Planning

Charitable planning allows you to support the organizations and causes that matter to you, while often providing immediate income streams and reducing your tax burden. Numerous charitable giving strategies exist, and we can help you design and execute a charitable giving strategy that is in alignment with your personal and philanthropic goals. Please seek tax advice from your own tax advisors.

Disability and Extended Care Needs

To execute a sound retirement strategy, asset and income protection are a must. Designing a plan that encompasses managing costs for extended periods of care and disability insurance can help create the necessary balance in a portfolio to ensure stability and protection of assets.

Products available through one or more carriers not affiliated with New York Life Insurance Company, dependent on carrier authorization and product availability in your state or locality.

Estate Planning

A well-engineered estate conservation plan can help minimize tax liability and ensure that loved ones are protected. I will work with you and your advisors to assess the impact of state and federal taxes on your estate and suggest strategies to help minimize those taxes while meeting your family’s needs. I do not provide tax advice.

Please consult with your own advisors for tax advice.

Wealth Management

Through Eagle Strategies LLC, a wholly owned subsidiary of New York Life Insurance Company, we work with our clients to design and implement a variety of wealth accumulation and management plans, offering investment programs ranging from separately managed portfolios of stocks and bonds to mutual funds, and access to third-party wealth management programs. We offer a consistent process to help ensure management of investment assets according to your goals, risk tolerance and time horizon. We then monitor your plan on a continual basis, and adjust and evolve as your needs change.

Financial Planning

Through Eagle Strategies LLC, we provide personalized financial planning to our clients that is specific to several variables, including their income, risk tolerance, values, and family. We work with each client to identify and prioritize their goals, explore options, establish effective strategies, construct and execute a plan, and assess the performance of the plan and make adjustments as needed.

Funding Buy-Sell Agreements

A buy-sell agreement is a legally binding agreement between co-owners of a business that governs the situation if a co-owner dies or leaves the business, whether by force or by choice. A funded cross-purchase buy-sell plan utilizes life insurance to help ensure that the arrangement is properly funded so that there will be money if the event occurs.

Funding Deferred Compensation

Deferred compensation is a written agreement between an employer and an employee in which the employee chooses to have part of his or her compensation withheld by the company, invested on their behalf, and distributed to them at a predetermined point in the future. Deferred compensation can be used as a flexible way to attract and incentivize key employees. We provide funding strategies for deferred compensation.

Executive Benefits

The success of most businesses is tied in to the talent, passion, and work ethics of their key executives. Executive benefit packages can help you attract, motivate, and retain high-caliber employees and keep your company healthy and stable. We can help you with funding non-qualified plans, supplemental employee retirement plans, split dollar plans, and more.

Key Person Insurance

Key person life insurance offers a death benefit that helps indemnify an employer for the loss of one of its most important assets—the key person. This can help assure continuity of the business for employees, customers, and creditors, and protects against losses in sales, momentum, and credit. It can also be used to assist with recruiting and developing a replacement for the employee.

Succession Planning

Succession planning allows owners to retire from their business within their own time frame, while preparing for the company to be transferred to family members, key employees, an outside party, or even a charity. This must be done in a way that achieves personal financial security, maintains harmony, and achieves maximum value for the business. We can provide financial strategies for succession planning.

Investment Advisory

Managing your wealth requires a clear understanding of your overall investment objectives. Eagle's comprehensive investment advisory capabilities utilize a disciplined investment approach that looks beyond traditional asset allocation, while addressing important factors such as risk tolerance levels and investment time horizons, to provide a clearer picture of our clients’ overall wealth.

Financial Planning

A comprehensive financial analysis of assets, liabilities, cash flow, and investments helps us identify a clear path to our clients’ prosperous futures. We’ll craft a detailed financial plan that helps you have the right wealth accumulation and preservation strategy in place to achieve your long-term investment objectives. More importantly, we continuously monitor and adjust our clients’ financial plans to ensure that they remain aligned with their stated objectives.

Fund Advisory Program

This program combines the expertise of professional third party investment managers with the personalized service and guidance of the Financial Advisor. By analyzing your overall investment goals, risk tolerance levels, and liquidity needs, we’ll help you determine which investment portfolio allocation, consisting of an optimal blend of nonproprietary mutual funds and/or exchange-traded funds (ETFs) is most appropriate for your investment goals and specific situation.

Separately Managed Accounts

Separately Managed Accounts (“SMAs”) are a type of professionally managed investment account that invest in individual securities on a discretionary basis and provide clients with the flexibility of restricting the holding of certain securities and tactically utilizing gains and losses for tax planning purposes. We will leverage Eagle’s robust offering of nonproprietary SMA strategies available through third-party money managers to either custom design a holistic investment portfolio or utilize individual strategies to address your specific allocation needs.

Rep Directed Program

This is an investment advisory program through which we will construct a customized portfolio of individual mutual funds, exchange traded funds (ETFs), and in some cases, individual securities, using the strategic asset allocation framework developed by Eagle Strategies and a leading institutional asset manager, or simply by us for you to review and approve. We’ll seek to utilize an optimal blend of asset classes that helps maximize long-term returns, manage overall portfolio volatility and achieve investment objectives while remaining aligned with your risk profile.

Whole Life

Whole life insurance is also known as permanent insurance. You receive coverage for your entire life, as long as premiums (which are a set amount per period) are paid. Whole life policies accumulate cash value tax-deferred.

Term Life

Term life policies provide coverage for a specific amount of time—such as five years, 10 years, or 20 years. Term premiums are often less expensive than whole life premiums, but once the term of the policy is complete, coverage terminates. There is no accumulation of cash value.

Universal Life

Universal Life insurance is designed to offer customizable death benefit protection with non-guaranteed planned premiums and a non-guaranteed death benefit. Depending on the product selected and the amount of premium you pay, Universal Life insurance can allow you to keep your coverage as long as you need: to age 80, 90, 100 or longer. Because of the policy’s flexible and non-guaranteed nature, it is important to fund your policy properly and actively manage your policy to reflect changes in interest crediting rates and policy charges over the duration of your policy. This policy will terminate if at any time the cash surrender value is insufficient to pay the monthly deductions. This can happen due to insufficient premium payments, if loans or withdrawals are made, or if current interest rates or charges fluctuate.

Variable Universal Life

Variable Universal Life Insurance combines the premium and death benefit flexibility of a universal life policy with investment opportunities. You may allocate your premium among a variety of professionally managed investment divisions plus a fixed account. Of course, with investment opportunities comes risk along with the potential for reward.

These products are offered by prospectus through NYLIFE Securities LLC. (member FINRA/SIPC), and a Licensed Insurance Agency.

Survivorship Life

Survivorship Life insurance—available as whole life, universal life, or variable universal life —covers two people and provides payment of the proceeds when the second insured individual dies. Survivorship life insurance is often used to help meet estate planning or business continuation goals.

Fixed Deferred Annuities

With a fixed deferred annuity, the interest rate on your policy is guaranteed never to fall below a certain amount.* For many people, this provides a measure of security.

( A fixed deferred annuity is subject to a sales charge for early withdrawals, which may be subject to income tax. Withdrawals prior to age 59½ are subject to a 10% tax penalty.)

*Guarantees are dependent upon the claims-paying ability of the issuing insurer.

Lifetime Income Annuities

A lifetime income annuity is an annuity in which income payments begin one period after the annuity is purchased. It is designed to provide you with predictable income monthly, quarterly, semiannually, or annually, no matter how long you live, and regardless of how the financial markets perform.

All guarantees associated with annuity contracts are based on the claims-paying ability of the issuing insurance company. Withdrawals may be subject to regular income tax, and if made prior to age 59½, may be subject to a 10% IRS penalty. In addition, surrender charges may apply.

Variable Deferred Annuities

A variable deferred annuity offers the advantage of tax deferral and can be used to accumulate money for retirement. The policy's accumulated value—and sometimes the amount of monthly annuity benefit payments—fluctuates with the performance of your variable investment account options. There are fees, expenses, and risks associated with the contract. Please be aware that assets allocated to the investment divisions are subject to market risks and will fluctuate in value.

Offered through NYLIFE Securities LLC (member FINRA/SIPC), and a Licensed Insurance Agency.

Estate Planning

As a farm owner, you should not only be thinking about the present, but also planning for the future. Your farmland is not a liquid asset and because of that, settlement problems may arise. The best way to ensure a smooth transition from one farm owner to the next is by estate planning. Essentially this is a framework for the disposition of your assets at the time of death. It will not only protect your land, but will also provide for the needs of your family and may help reduce high inheritance taxes. By creating an estate plan, you can go forward knowing that your farm and your family will always be in good hands.

We do not provide legal or tax advice. Please consult with your own advisors for legal and tax advice.

Succession Planning

When it comes to passing on a farm and all that comes with it, farm owners have many important decisions to make. Farmland can be passed on to relatives, employees, outside parties, and even charities. Even after this decision is made, however, many more remain. Succession planning with our team means making these decisions together and making sure your farm has the resources it needs to remain economically sound and continue with the legacy you desire

Asset Protection

Protecting your assets means getting to know you, your values, and your priorities. Asset protection allows us to work with you to plan for the future, protect your farm and personal assets, such as wealth, future income, and guide the process of transferring assets to future generations.

Charitable Planning

When a charity or organization matters to you, it also matters to us. We’re here to help support your philanthropy by creating a financial strategy that includes charitable giving in its budget. In many financial strategies, even giving, our team of professionals can help you make the most of your decisions.

Buy-Sell Agreements

A buy-sell agreement is a legally binding contract between co-owners of a farm that sets a plan in place in the event of one owner’s death or departure from the business, regardless of the circumstances. Essentially, it provides a protected way out of farm ownership if the necessity arises. Our team works with you to employ life insurance to fund a buy-sell agreement, so that the business will not struggle financially even in the case of a co-owner’s death.

Key Person Considerations

A farm is only able to run at its best when all of the employees and owners work together and share common goals. But what happens when a key member of the team passes away? That’s where our company can help, by insuring the key person with life and disability insurance that will help compensate the farm owner in the event of a loss. Key-person insurance can help protect the farm from a loss of sales, credit, and workforce. Is there one employee you cannot imagine working without, who contributes invaluable skills and ideas? If so, we can help you protect your farm even in the case of this worker switching employers, becoming disabled, or dying.

Individual disability insurance is available through one or more carries not affiliated with New York Life Insurance Company, depending on carrier authorization and product availability in your state or locality.